Will You Get Paid Sooner If You Make A Car Finance Claim Now

Recent coverage featuring Martin Lewis has brought fresh attention to mis-sold car finance. A key takeaway is simple. If you think your agreement was not properly explained, raising a complaint now could mean your case is reviewed sooner.

This is not about rushing or assuming you are owed compensation. It is about understanding how the timing of your complaint can affect where you sit in the process.

Why Timing Can Influence Your Claim

The Financial Conduct Authority is reviewing discretionary commission arrangements, often referred to as DCAs. These allowed some brokers and dealers to increase the interest rate on your finance agreement to earn more commission. In many cases, this was not clearly explained to customers at the time.

Because of this, lenders are preparing for a high volume of complaints. Some have already seen a sharp increase in cases being raised.

If you submit your complaint now, it is logged earlier and enters the system ahead of others who may wait. This does not change the outcome of your complaint, but it can affect how quickly it is picked up and reviewed.

If a large number of complaints are submitted later, delays are more likely. Being earlier in the process can help reduce that risk.

What The Current Update Means In Practice

Recent reporting suggests that up to 12.1 million car finance agreements could be affected, particularly those taken out before January 2021, when the rules around commission changed.

You do not need to wait for the FCA to complete its review before taking action. If something about your agreement was unclear, or you were not given enough information to make an informed decision, you can raise a complaint now.

This is important because any wider compensation scheme may rely on complaints already being logged. While this is not guaranteed, being in the system early can help ensure your case is considered without added delay.

Understanding Discretionary Commission In Simple Terms

Discretionary commission meant that the dealer arranging your finance could influence the interest rate you were offered. A higher rate often meant a higher commission for the broker.

What matters is whether this was clearly explained to you. You should have been given enough information to understand how the rate was set and whether the dealer had any financial incentive linked to it.

If that was not made clear, you may have grounds to question whether the agreement was fair and transparent.

When You May Want To Check Your Agreement

Many people are now looking back at their finance agreements to see if anything was unclear at the time.

This may apply to you if you took out a PCP or HP agreement before January 2021 and do not recall the commission structure being explained. It may also be relevant if the interest rate seemed high compared to what you expected, or if you were not offered alternative finance options.

You do not need to have full documentation or detailed evidence before raising a complaint. A clear concern about how the agreement was presented is enough to begin the process.

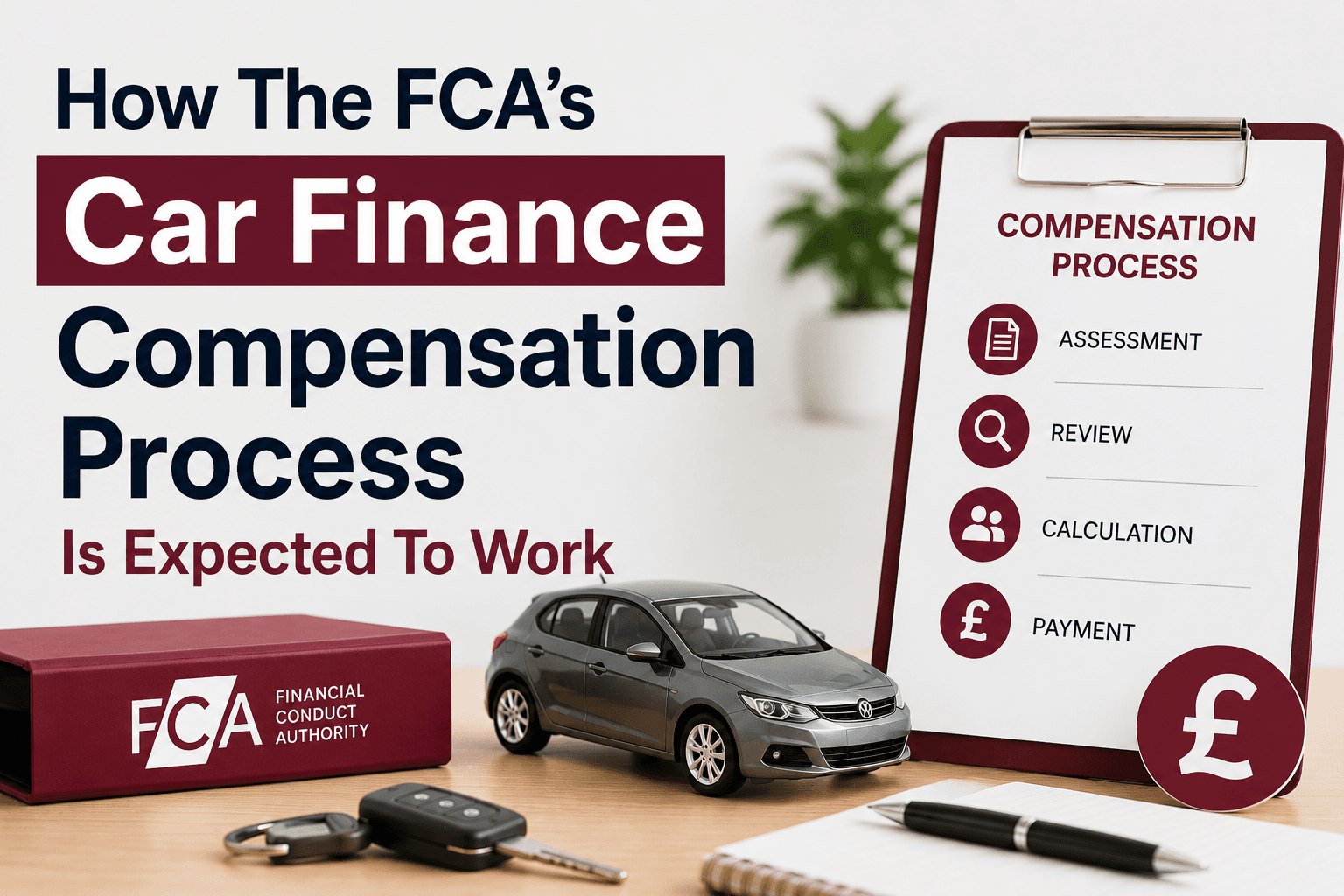

What Happens After You Raise A Complaint

Once you contact your lender, they will review your complaint. This response should explain whether they believe the agreement was fair and whether any compensation is due.

Some complaints may be paused while the FCA continues its review. This is part of a wider process and does not mean your complaint has been dismissed.

Importantly, your complaint is still recorded. If there is a broader industry decision on compensation, having your complaint already in place may help move your case forward more quickly than if you had waited.

Why Complaining Now Can Be A Practical Step

Raising a complaint now is about putting your case in motion. It ensures your concerns are formally recorded and allows your lender to review your agreement.

If complaint volumes continue to rise, those who wait may face longer processing times. By acting earlier, you reduce the risk of being caught in a backlog.

There is no requirement to wait for further announcements if you already believe your agreement was not clearly explained.

Do You Need To Use A Claims Company

You can submit a complaint directly to your lender at no cost. The process is designed to be accessible and does not require legal or specialist support.

Claims companies will usually follow the same process on your behalf. They do not have the ability to speed up the outcome of your complaint. Using a third party may reduce the amount you receive if fees are deducted from any compensation.

For many people, raising a complaint themselves is a straightforward and practical option.

Taking A Balanced View

It is important to keep expectations realistic. Not all car finance agreements were mis-sold, and not every complaint will result in compensation.

However, if you have a genuine concern about how your finance was explained, raising a complaint now allows your case to be considered at the earliest stage possible.

This approach is about being informed and prepared, rather than waiting for certainty that may take time to arrive.

How Mis-Sold Expert Can Help

Mis-Sold Expert helps you understand your rights if you think your car finance was not explained properly. We provide clear, practical guidance so you can decide what to do next.

You can claim without using a claims management company; you can go to your finance provider and then to FOS, for free. Additionally, the FCA is introducing a free consumer redress scheme.