The FCA Car Finance Investigation: What It Means for Your Claim

FCA Car Finance Investigation 2024–2026: What It Means for PCP and HP Agreements

Over the past year or so, the spotlight has really been shone on just how car finance agreements were sold here in the UK. People are increasingly concerned about how commissions were arranged, how interest rates were set, and how transparent it all was. It's all leading to the FCA carrying out a review of car finance that will run from 2024 to 2026. This review is now having a significant impact on how complaints and claims are assessed across the motor finance industry.

Car finance has become one of the most common ways to buy a new car in the UK. Loads of drivers rely on finance agreements arranged through dealerships to spread the cost of a car out over several years. Personal Contract Purchase (PCP) and Hire Purchase (HP) agreements have been the market leaders for more than a decade.

In this time, lenders have been paying commissions to dealerships or brokers on many finance agreements they have agreed. Commission is normal, and it's used in loads of other financial services sectors. But questions have been raised about how these commission systems operated and whether customers were ever fully aware of how the interest rates actually worked.

The regulators are particularly interested in situations where the commission paid to the broker was tied to the interest rate applied to the finance agreement. This system is known as discretionary commission and was widely used across the car finance industry before some regulatory changes were implemented in 2021.

The Financial Conduct Authority (FCA), which is responsible for regulating consumer credit and financial services in the UK, is now going back and looking at these older arrangements. They want to know if customers were given clear information at the time they agreed to the finance deal and if firms actually met the regulatory standards around fairness and transparency.

If you've taken out a car finance deal in the past, especially if you went through a dealership, you might be wondering what this investigation all means for you. This guide aims to give you a clear idea of what the FCA investigation is all about, which lenders are affected, how the old commission system worked and how the complaints process usually works.

The idea is to provide clear and factual information so you can make sense of the situation and decide for yourself whether you might want to take a closer look at your own agreement.

What the FCA Car Finance Investigation Is

The FCA car finance investigation is a market review examining how commission arrangements operated when car finance agreements were sold between 2007 and January 2021.

During this period, many finance agreements were arranged through dealerships acting as credit brokers. The dealership would introduce the customer to a finance provider and receive commission from the lender when the agreement was completed.

The FCA’s investigation is examining whether certain commission structures created incentives that may have influenced the interest rate charged to consumers. In particular, the regulator is reviewing discretionary commission arrangements where brokers had the ability to increase the interest rate on a loan within a permitted range.

The investigation focuses on several key questions:

- How widely was discretionary commission used across the motor finance market

- Whether customers were informed about how the commission operated

- Whether the commission influenced the cost of finance

- Whether lenders had appropriate controls over broker behaviour

- Whether customers were treated fairly during the sales process

The FCA banned discretionary commission models in January 2021 because of the potential conflict of interest between dealers and consumers.

However, many agreements arranged before the ban remain active or were only repaid recently. As a result, a significant number of consumers have raised complaints about whether their finance agreements may have been affected.

The FCA launched this review to ensure that complaints are handled consistently and fairly across the market.

Importantly, the investigation does not assume that all car finance agreements were mis-sold. Instead, it aims to determine whether certain practices may have led to unfair outcomes for some consumers.

Why Commission Has Become a Key Issue

Commission is a standard part of many credit broking arrangements. When a dealer arranges finance through a lender, the lender usually pays the dealer a commission for introducing the customer.

In many cases, this commission is fixed and does not affect the interest rate offered to the consumer.

However, the FCA investigation focuses on situations where commission may have influenced the cost of borrowing.

Under discretionary commission models, lenders set a base interest rate for the finance agreement. Dealers were then allowed to increase that rate within a defined range.

For example:

- A lender might set a base interest rate of 6%

- The dealer could increase the rate to 7% or higher

- The dealer’s commission would increase alongside the higher rate

This meant that a dealer could potentially earn more commission by offering a higher interest rate.

From the customer’s perspective, the interest rate appeared as part of the finance offer. Many consumers may not have been aware that the dealer had the ability to adjust the rate within a permitted range.

The FCA concluded that this structure created a potential conflict of interest. Dealers could have an incentive to increase the interest rate even though a lower rate would reduce the overall cost of finance for the customer.

For this reason, discretionary commission models were banned from January 2021.

The FCA investigation is now reviewing historical agreements to determine whether the use of these arrangements may have resulted in unfair outcomes for consumers.

Which Lenders Are Affected

The FCA investigation into the UK motor finance market covers a wide range of lenders that operated during the period under review.

This includes both large banks and specialist motor finance providers.

Examples of lenders commonly associated with the car finance sector include:

- Black Horse Finance

- Santander Consumer Finance

- Barclays Partner Finance

- Close Brothers Motor Finance

- Volkswagen Financial Services

- BMW Financial Services

- Mercedes-Benz Financial Services

- MotoNovo Finance

- Moneybarn

- PSA Finance

- Toyota Financial Services

- Ford Credit

- Nissan Finance

- Vauxhall Finance

These lenders have provided finance products to customers through dealership networks across the UK.

However, the inclusion of a lender in discussions about the investigation does not mean that all of their agreements involved discretionary commission.

Many lenders used a range of commission models over time. Some agreements may have involved discretionary commission, while others used fixed commission or flat-fee arrangements.

The FCA investigation focuses on how commission structures operated rather than targeting individual lenders.

Each agreement must be considered individually, taking into account the details of the finance terms and the sales process involved.

What is Discretionary Commission

Discretionary commission is a type of commission structure where the dealer or broker has the ability to influence the interest rate that the customer gets charged.

In a typical car finance transaction, there are three parties involved, the consumer buying the car, the dealer acting as the broker, and the finance lender who provides the credit.

When discretionary commission models were used, the lender would set a base interest rate for the finance product, and the dealer would have the freedom to increase that rate within a specified range.

The difference between the base rate and the rate charged to the customer would then generate additional commission for the dealer.

Here's an example to make it a bit clearer :

- Lender base rate: 6%

- The dealer increases the rate to 8%

- The extra 2% helps to pad the dealer's commission

The higher the interest rate that is applied to the agreement, the more commission the dealer gets. Customers are often presented with the interest rate as part of the finance quote, but they might not necessarily know why the rate was chosen.

This lack of transparency raised some serious questions.

The FCA decided that linking commission directly to the interest rate created a risk that customers might not get the most competitive finance option available.

That's why discretionary commission arrangements were eventually banned from January 2021 onwards.

What Types of Finance Are Involved

The FCA investigation mainly focuses on car finance agreements that were arranged through dealerships or brokers.

Two types of finance are particularly relevant here.

Personal Contract Purchase (PCP)

PCP is probably one of the most commonly used car finance products in the UK.

A typical PCP agreement will include things like :

- An initial deposit

- Monthly payments over a fixed term

- A final optional payment known as a balloon payment

At the end of the agreement, the customer can choose to pay the final amount to keep the car, return the vehicle, or use the car's value as a deposit for another vehicle.

PCP agreements can be a bit more complicated than other types of finance because they involve multiple cost components, like residual value calculations and optional final payments.

That's one reason why PCP agreements have been in the spotlight when it comes to hidden commission concerns.

Hire Purchase (HP)

HP agreements are a bit simpler.

Under HP finance :

- The customer pays a deposit

- Monthly payments are made over a fixed term

- Once the final payment is made, the customer gets ownership of the car

HP agreements don't include a balloon payment, but they still involve interest rates and commission payments to brokers, which puts them in scope of the FCA investigation if discretionary commission was involved.

Who Can Claim

Not every car finance customer will have grounds to make a complaint. However, some agreements may be worth taking a closer look at.

You might be able to raise a complaint if :

- Your car finance agreement was arranged before January 2021

- The financing was arranged through a dealership or broker

- The interest rate may have been influenced by discretionary commission

- Commission arrangements weren't clearly explained

Transparency is the key here. Customers should have been told exactly how their finance was structured and how costs were determined.

If important details were not explained, it may raise questions about whether the sales process met regulatory expectations.

And just to be clear, the commission itself is not automatically unfair. Many agreements included commission that was fixed and clearly disclosed.

A complaint usually focuses on whether commission influenced the interest rate and whether the customer was told about this.

Each case has to be looked at individually based on the evidence available.

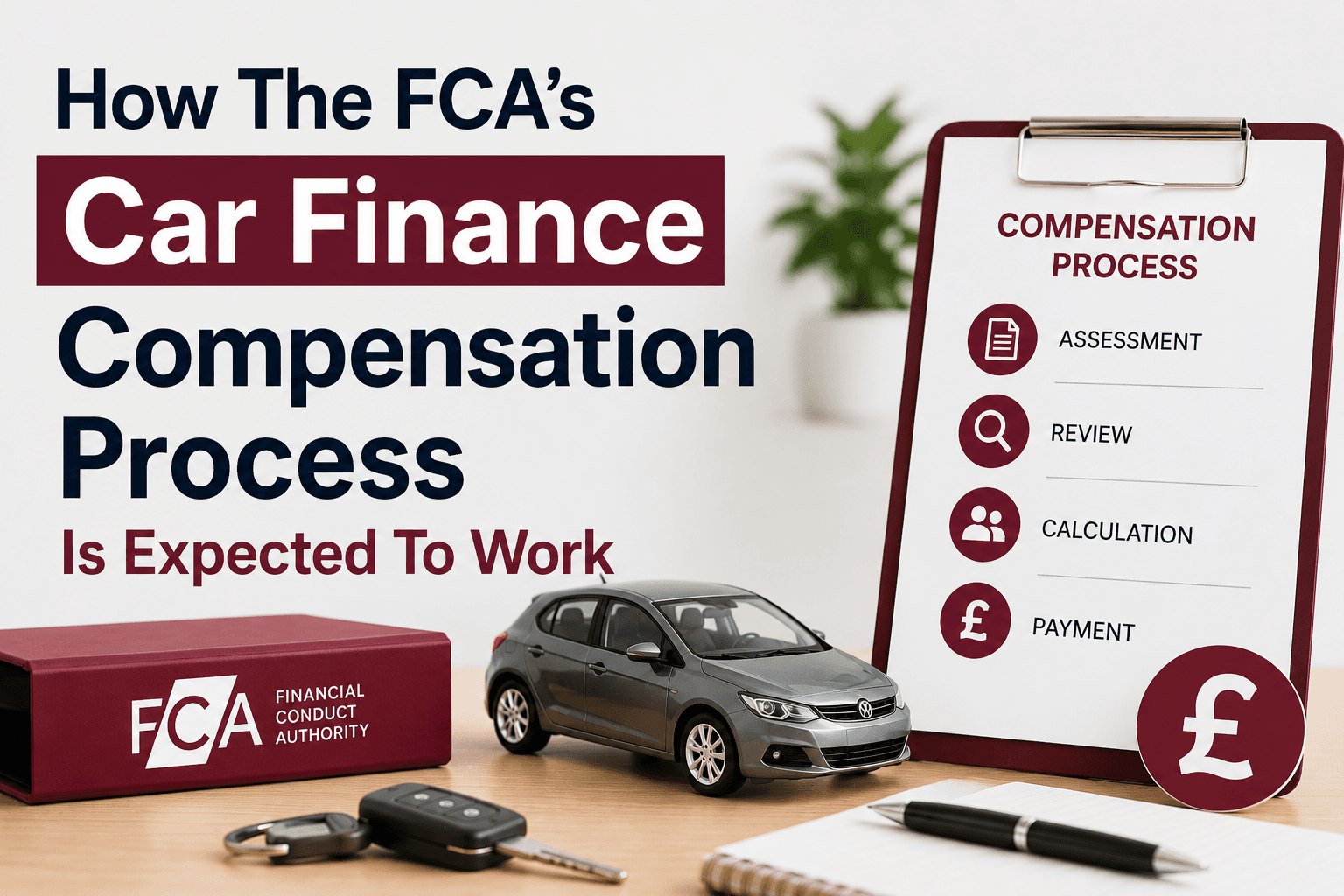

How Much Compensation You Could Get

Compensation in car finance complaints aims to get the consumer back into the financial position they would have been in if the issue had not occurred.

The amount varies greatly depending on the details of the agreement.

Some factors that might influence compensation include :

- The interest rate that was applied

- The base interest rate that could have been offered

- The size of the finance agreement

- The length of the loan term

If a complaint is upheld, compensation may involve :

- Refunding excess interest paid IN - the lender will treat you fairly when it comes to the interest you've paid back, adjusting the outstanding balance on the loan

- Adjusting the outstanding balance on the loan - essentially reducing the amount you still owe

- Adding statutory interest to refunded amounts - an extra amount on top of the main refund

In some cases, the amount of compensation might be pretty small, but for others, the difference could be a lot larger depending on just how much interest rates increased.

There's no one-size-fits-all here; the amount of compensation will depend on the specifics of your case.

The FCA investigation may help clarify the rules around calculating compensation once they've finished reviewing it all.

Claim Deadlines

Financial complaints in the UK generally have a deadline, set by the Financial Ombudsman Service.

You've normally got:

- Six years to complain from the event

- Or three years from when you first spotted the issue

though the FCA has introduced some temporary measures while it takes a closer look at the motor finance market.

This has put a temporary hold on complaints about discretionary commission, till the regulator issues some further guidance.

The lenders need time to get their heads around how to handle these complaints fairly, while the FCA gets to the bottom of things.

Even though the FCA review might shake things up a bit, it's still a good idea to review your agreement sooner rather than later if you've got concerns

Step-by-Step Car Finance Claim Process

If you want to have a closer look at your car finance agreement, and maybe even make a complaint, the process generally follows a few stages.

Step 1: Review Your Agreement

First things first, grab all the documents you have relating to the finance agreement.

This may include:• the credit agreement• the paperwork you got before signing the contract• any dealerships documents• your payment statements

Have a good look at:• the interest rate• the total amount you agreed to pay• any mention of commission or broker fees

understanding these things can help you figure out how the agreement was structured in the first place

Step 2: Submit a Complaint to the Lender

If you think the agreement wasn't explained to you very clearly, you can submit a complaint to the finance provider.

They are responsible for sorting out complaints about the credit agreement.

You can either get in touch with them directly or get a claims management company to help you with the complaint

Step 3: Investigation by the Finance Provider

The lender will take a close look at your complaint and decide what to do.

This may involve checking over:• the finance agreement• any records from the dealership• how the lender earns its commission• what was said to you when you signed up

they'll then decide whether your complaint is legitimate or not

Step 4: Final Response

The lender will then send you a written response explaining their decision.

If they agree with you, they'll tell you how much compensation they're offering.

If they reject your complaint, they should explain why and give you some background on how they came to that decision

Step 5: Financial Ombudsman Review

If you don't like the lender's response, you can get the Financial Ombudsman Service to take a look.

The Ombudsman reviews complaints between consumers and financial firms - and makes their own decision based on what you've both said.

Why Outcomes Will Vary Between Cases

Car finance agreements are all over the place when it comes to structure, interest rates and how they're sold.

That makes it tough to predict how any given complaint will be resolved, because every case is different.

The type of finance you've got, when you signed up for it, the commission model used and how the agreement was explained to you are all things that could affect the outcome of your complaint

Because of that, complaints are dealt with one at a time, and not with some blanket policy

What the FCA Investigation Does and Does Not Mean

The FCA investigation has certainly highlighted some potential issues with how car finance works, but it's worth remembering that it doesn't mean every car finance agreement was mis-sold.

Nor does it automatically mean you'll receive a refund.

What the FCA is actually trying to do is figure out if certain commission structures put customers at a disadvantage.

Many finance agreements were sold honestly and in line with the rules.

The investigation is looking to ensure that complaints about these agreements are sorted out fairly and consistently

What Consumers Should Do Now

If you've got a car finance agreement and are wondering if it might be affected by the FCA investigation, it's a good idea to take a close look at your documents.

You might want to check:

- When you signed up for the finance

- The interest rate you were charged

- Whether commission was mentioned

- How well you were informed about the finance

understanding these things will help you decide whether to raise a complaint or ask the lender for more info

Looking Ahead

The FCA car finance investigation is part of the broader effort to make the financial services industry more consumer friendly.

In recent years, regulators have put more emphasis on transparency and ensuring customers get clear information about the products they buy.

The findings of this investigation may influence how lenders sort out complaints and how car finance products are sold in the future.

For consumers, the most important thing is to understand how your agreement was arranged and whether you got a fair deal at the timeIf you've ever had car finance & later start to worry about how your interest rate was set or if your agreement was explained clearly, the FCA investigation might just provide the context you need.

It won't, however, decide on the outcome of your individual complaint, but it does drive home the point that when selling financial products , transparency & fair treatment are a must.

Taking a closer look at your finance agreement can help you get a better understanding of how the costs were broken down & whether you want to take things further.

If you suspect your car finance could've been explained in a way that wasn't quite right, Mis-Sold Expert is here to help you review your agreement & figure out what your options are.

You can claim without using a claims management company; you can go to your finance provider and then to FOS, for free. Additionally, the FCA is introducing a free consumer redress scheme.