FCA 39% Commission Threshold Explained: Could Your Car Finance Qualify?

One of the most important parts of the FCA’s car finance redress scheme is how it defines “high commission”.

This matters because not every car finance agreement will qualify for compensation. The FCA has introduced clear thresholds to identify when commission becomes significant enough that failing to explain it properly may have created an unfair relationship.

If you had car finance between 2007 and 2024, understanding these thresholds can help you assess whether your agreement may fall within the scheme.

What Is “High Commission” in Car Finance?

Commission is the payment made by the lender to the broker or dealer for arranging your finance. The FCA does not treat commission itself as a problem. The issue arises when it is large enough to influence the deal and is not properly disclosed.

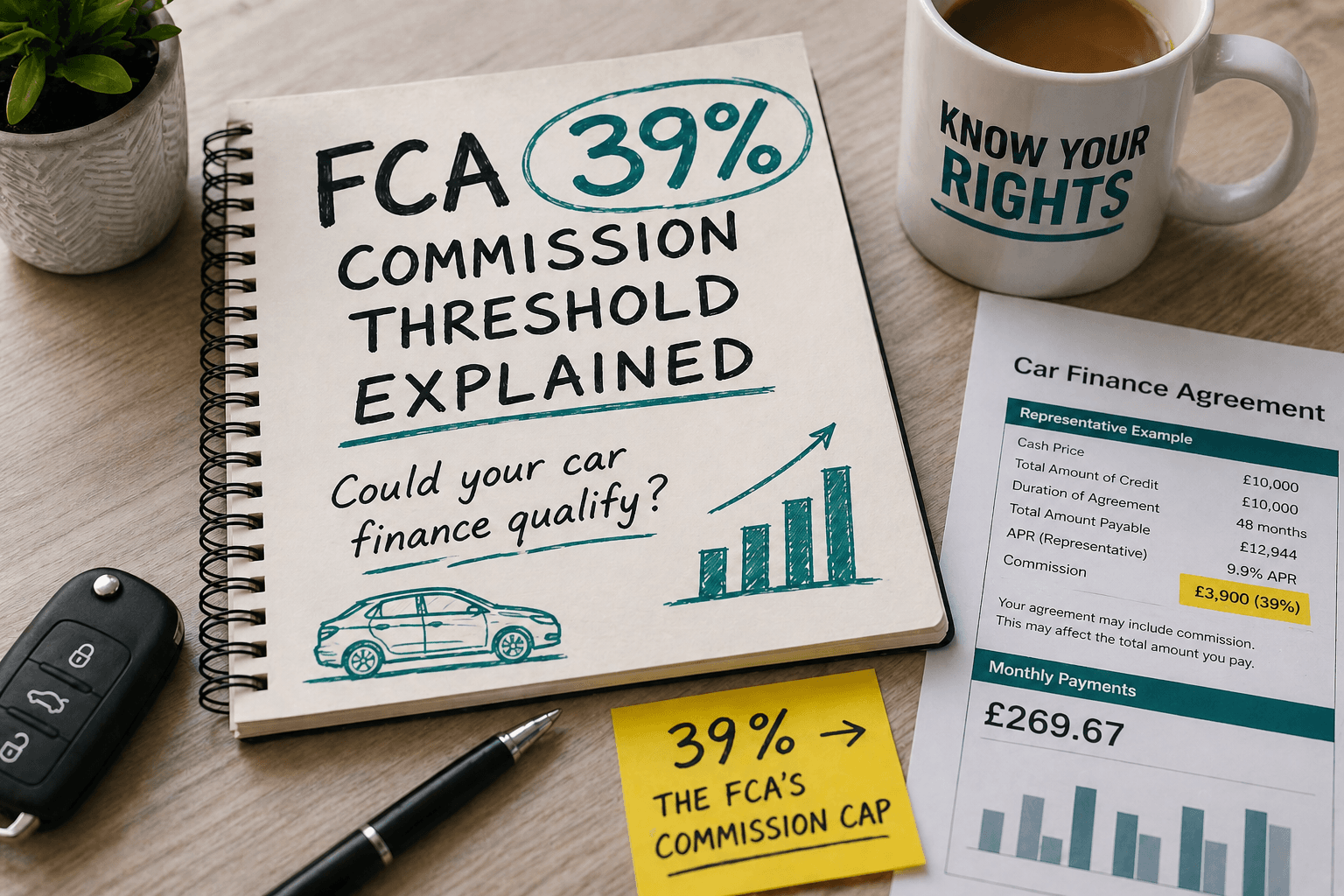

Under the FCA’s rules, commission is considered high when it meets two conditions at the same time. It must be at least 39% of the total cost of credit, and it must also be at least 10% of the total loan amount.

Both elements are required. This ensures the focus remains on agreements where commission is not only proportionally high but also meaningful in real terms.

Why the 39% Threshold Matters

The 39% figure reflects the FCA’s analysis of market data. It represents commission levels that sit well above typical arrangements and are more likely to have influenced how the finance was structured.

At this level, commission becomes a significant part of the cost of borrowing rather than a minor background cost. This increases the likelihood that it could have affected the interest rate you were offered or the lender selected on your behalf.

The FCA’s view is that, at this point, the existence and impact of commission would be important information for a customer making a decision. If that information was not properly explained, the relationship may be considered unfair.

Why the 10% Loan Threshold Is Also Important

The FCA did not rely on a single percentage because that could capture cases where commission appears high in theory but is relatively small in value.

By also requiring commission to reach at least 10% of the loan amount, the FCA ensures the threshold applies only where the financial impact is meaningful. This avoids including agreements where commission is technically high as a percentage of interest but does not materially affect the overall cost of the loan.

Together, these two thresholds create a more balanced test that focuses on cases where commission could realistically have influenced both the deal and your decision.

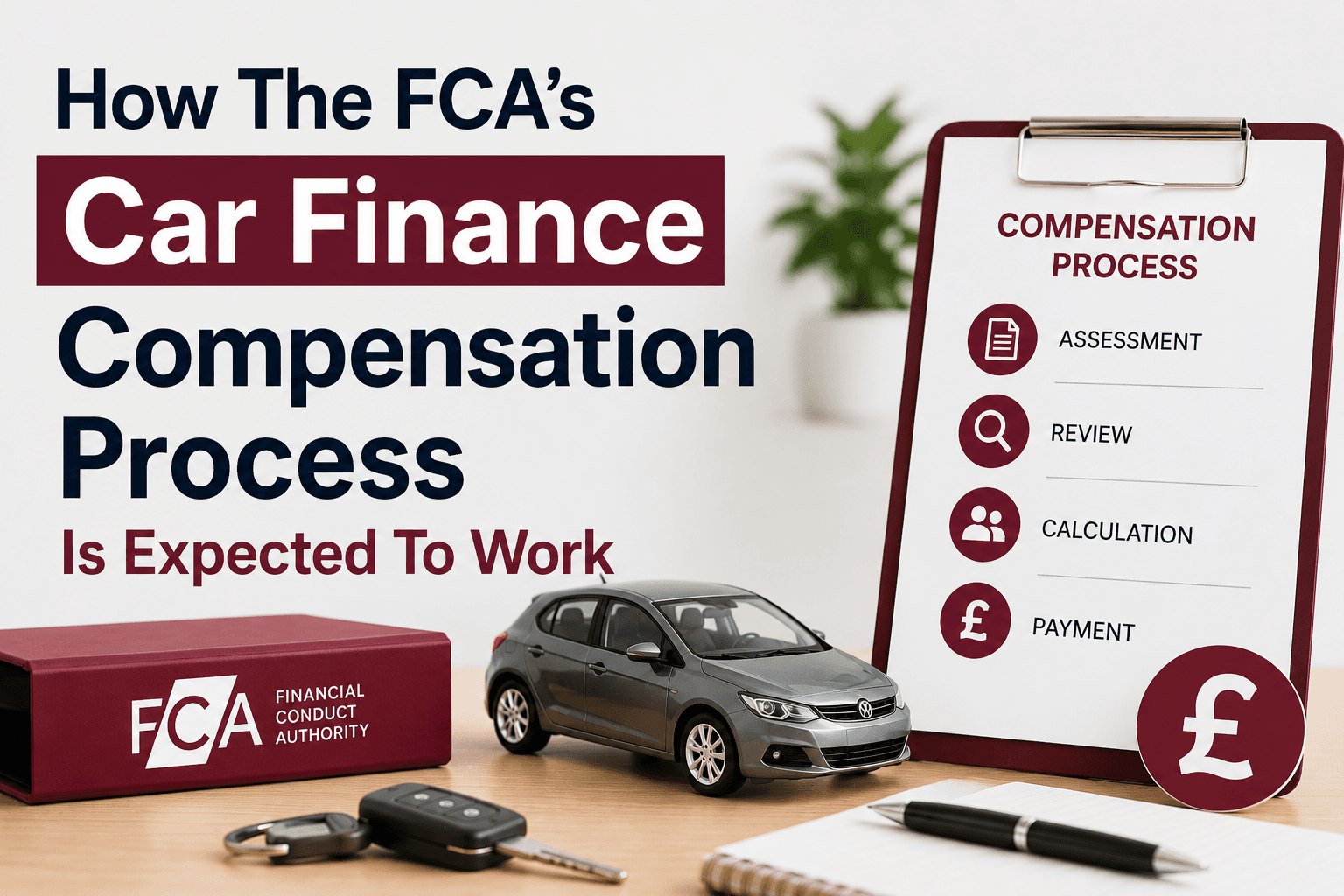

Does High Commission Automatically Lead to Compensation?

High commission is a key trigger within the scheme, but it does not automatically mean compensation will be paid.

The FCA’s focus is on whether the arrangement was adequately disclosed. If the commission was clearly explained, presented in a way you could understand, and gave you enough information to make an informed choice, the relationship may not be considered unfair.

However, the FCA has also recognised that disclosure across the market was often limited or unclear. In many cases, customers were not told about commission at all, or were given only general information that did not explain how it worked in practice.

This means that where high commission exists, there is a stronger likelihood that the agreement may fall within the scope of the scheme, depending on how it was presented at the time.

The Different Situations That May Qualify

High commission is only one part of the FCA’s framework. There are other types of arrangements that can also lead to compensation if they were not properly explained.

One of the most significant is the discretionary commission arrangement. In these cases, the broker had the ability to adjust your interest rate, and their commission increased as the rate increased. This created a direct conflict of interest, as the broker could benefit financially from charging you more.

Another situation involves tied or restricted relationships between lenders and brokers. If a broker was limited to offering finance from certain lenders, or had a preferential arrangement that influenced which deals were presented, this could affect your ability to access better options. If this was not disclosed, it may contribute to an unfair relationship.

There are also more extreme cases involving very high commission. Where commission reaches at least 50% of the total cost of credit and 22.5% of the loan amount, and is combined with other issues such as discretionary commission or tied arrangements, a higher level of compensation may apply.

When High Commission May Not Result in Compensation

Not all agreements involving commission will lead to compensation.

Where commission falls below the FCA’s defined thresholds, it is less likely to be considered significant enough to affect the fairness of the relationship. Similarly, if the deal you received was already highly competitive compared to the wider market, compensation may not be payable even if commission was present.

The FCA has also identified a group of agreements where consumers paid some of the lowest interest rates available at the time. In these cases, it considers that the outcome for the customer was already favourable, and redress may not be appropriate.

What This Means for You

The introduction of clear thresholds removes much of the uncertainty around what qualifies as high commission.

Rather than focusing simply on whether commission existed, the FCA’s approach looks at how large it was, whether it could have influenced the deal, and whether it was properly explained.

If your agreement involved commission at or above these levels and you were not given clear information about it, there is a stronger basis for it to fall within the scheme.

Why the FCA Set These Thresholds

The FCA’s aim was to create a framework that is consistent, fair, and workable across millions of agreements.

Without defined thresholds, every case would need to be assessed individually, which would lead to delays and inconsistent outcomes. By setting clear criteria, the FCA has made it easier for firms to identify affected customers and apply a standard approach to compensation.

This also helps ensure that the scheme focuses on cases where commission is most likely to have had a meaningful impact.

Understanding Your Own Agreement

Many people are unsure how their car finance was structured or whether commission played a role.

You can check your car finance agreement with Mis-Sold Expert to understand how your deal was set up and whether commission may have reached the levels identified by the FCA. We explain the key details in clear, practical terms so you can see how your agreement works and what it could mean for you.

You can also stay up to date with FCA announcements and wider industry developments, helping you understand how the scheme is progressing and what to expect next.

Mis-Sold Expert helps you understand whether your car finance agreement may have been mis-sold. We explain your options clearly so you can decide what to do next, based on your own circumstances.

You can claim without using a claims management company; you can go to your finance provider and then to FOS, for free. Additionally, the FCA is introducing a free consumer redress scheme.