Barclays Car Finance Compensation: What the FCA Redress Scheme Could Mean for You

Barclays has set aside around £325 million following regulatory developments linked to historic car finance commission arrangements. The Financial Conduct Authority is now developing an industry-wide redress scheme covering certain motor finance agreements taken out between 6 April 2007 and 1 November 2024.

If you arranged PCP or HP finance through a dealership during that period, your agreement may fall within scope. Whether you qualify depends on how the commission was structured and disclosed at the time.

The scheme is expected to open in early 2026, subject to consultation and final FCA rules.

Why Barclays Has Increased Its Provision

Barclays increased its provision following the FCA's confirmation of an industry-wide motor finance redress scheme addressing historic undisclosed commission arrangements in Personal Contract Purchase (PCP) and Hire Purchase (HP) agreements.

The FCA estimates that around 14 million motor finance agreements entered into between 2007 and 2024 could fall within the scope of the scheme. The regulator expects lenders to review affected agreements and compensate customers where undisclosed commission arrangements caused financial loss.

The FCA estimates the scheme will return approximately £7.5 billion to consumers across the UK. While compensation will vary according to individual circumstances, the regulator's current estimates suggest average payments of around £829 per eligible agreement.

Barclays' provision increase reflects both the FCA's final redress framework and ongoing legal developments relating to motor finance commission disclosure. The bank has stated that uncertainty remains around the final cost of compensation, customer participation rates and the practical implementation of the scheme. As a result, the ultimate financial impact could differ from the amount currently set aside.

How Commission May Have Affected You

When you take out PCP or HP finance, you agree to a deposit, fixed monthly repayments and interest charged at an agreed rate. In many cases, you deal directly with the dealership rather than the lender.

If your agreement involved a discretionary commission arrangement, the dealer may have had influence over the rate you were offered. You may not have been told that the dealer could adjust that rate or that their commission depended on it.

That does not automatically mean your agreement was mis-sold. The FCA’s review focuses on whether the structure created unfair outcomes or breached consumer credit rules.

The wider review also considers other commission models where payments to dealers may not have been clearly explained. The key issue is transparency and whether you paid more because of the way commission worked.

Who May Qualify For Mis-Sold Car Finance Compensation

The FCA has proposed that certain agreements taken out between 6 April 2007 and 1 November 2024 could be reviewed under a standard redress framework.

You may fall within scope if your PCP or HP agreement was arranged through a dealership or broker and commission was paid by the lender to the dealer. Eligibility depends on the specific commission structure used and what you were told at the time.

Major lenders across the sector are involved, including Barclays, Lloyds Banking Group, Santander, Close Brothers and others. The FCA’s aim is to apply a consistent approach across firms.

Not all agreements will qualify for compensation. Some may show no financial loss. Each case will depend on its individual facts and the final methodology confirmed by the FCA.

What Compensation Could Include

Where redress is due, it is expected to focus on financial detriment rather than penalties.

The FCA states - "This would include interest, which is normally paid on top of compensation. This would be based on the average base rate per year, plus 1% from the date you made the overpayment to the date compensation is paid."

Some industry commentary has suggested that redress in certain upheld complaints has averaged several hundred pounds per agreement. Actual outcomes vary. The size of the loan, the interest rate applied and the term length all affect any calculation. Some agreements may result in no compensation if no overpayment is identified.

Legal Developments and Court Decisions

Barclays has been involved in legal proceedings connected to commission disclosure and Financial Ombudsman Service decisions.

In April 2024, Barclays sought a judicial review of an ombudsman decision concerning commission disclosure. In December 2024, the High Court rejected that challenge.

Separately, commission-related cases involving multiple lenders have progressed to the Supreme Court. Those appeals may clarify certain legal principles around disclosure and duties owed to customers. The FCA has chosen to consult on a broad redress scheme to provide consistency rather than rely solely on case-by-case decisions.

The regulatory position continues to develop. Final rules will determine how eligibility and compensation are assessed.

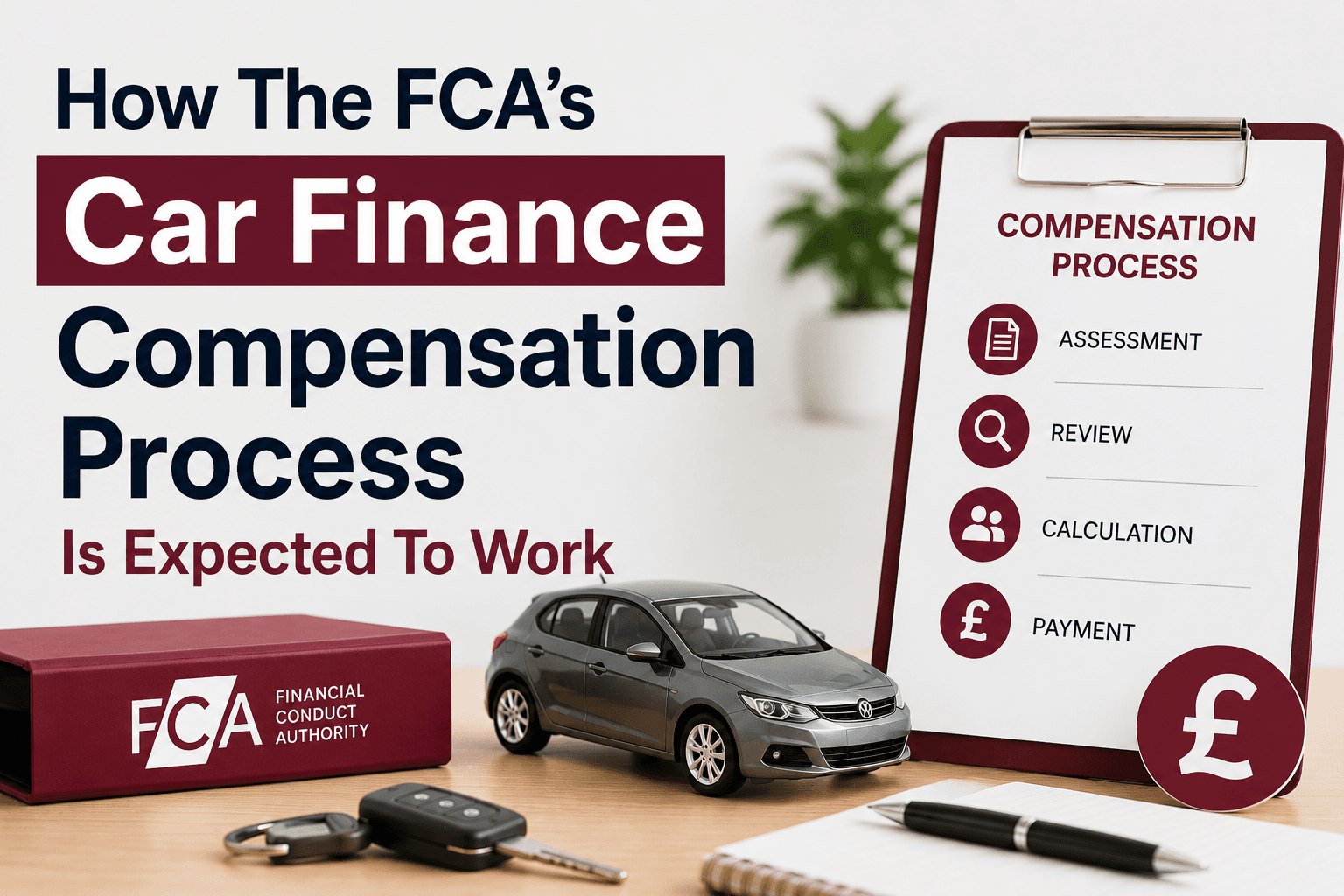

How the FCA Redress Scheme Is Expected to Work

The FCA has proposed a single industry-wide scheme so you do not face different processes depending on the lender.

Once the framework is finalised, you would raise a complaint directly with your lender. The lender would assess whether your agreement falls within scope. If it does, redress would be calculated using a standard methodology set by the FCA. Payment would follow where compensation is due.

The scheme is expected to open in early 2026, subject to consultation outcomes and final confirmation. Customers who have already complained may have their cases reassessed once the complaint handling pause lifts.

Key Dates So Far for Mis-sold Car Finance Claims

The proposed start date for agreements within scope is 6 April 2007. Discretionary commission arrangements were banned in January 2021. The FCA launched its formal review into the motor finance commission in January 2024.

Judicial review proceedings involving Barclays took place in April 2024, with the High Court rejecting the challenge in December 2024. Consultation on the wider redress scheme is expected to conclude in March 2026 with the FCA scheduled to announce an update imminently, with implementation anticipated in early this year, subject to final FCA rules.

What You Can Do Now

You do not need to take urgent action while the consultation continues. If you want to prepare, you can review any car finance agreements you entered into since 2007 with Mis-Sold Expert or other claims management companies. Check whether they were PCP or HP and whether they were arranged through a dealership.

If you still have copies of your finance agreements or settlement letters, keep them accessible. If not, lenders may still hold records.

Raising a complaint about historic commission structures generally relates to pricing and disclosure rather than missed payments. In most cases, this does not affect your credit file. Individual circumstances can differ.

Not every agreement will qualify for redress. Eligibility depends on the commission model used, the disclosure provided at the time and the FCA’s final rules.

You can claim without using a claims management company; you can go to your finance provider and then to FOS, for free. Additionally, the FCA is introducing a free consumer redress scheme.